HMRC will reduce its late payment and repayment interest rates from today (28 May), following the Bank of England’s recent decision to cut the base rate by 0.25%.

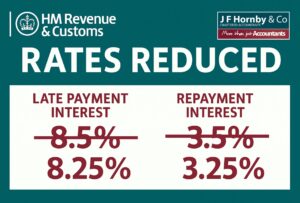

The base rate fell from 4.5% to 4.25% on 8 May, prompting an automatic adjustment to HMRC’s linked rates. As a result, the late payment interest rate will fall from 8.5% to 8.25%—still one of the highest rates seen since February 2000.

Meanwhile, the repayment interest rate, which HMRC pays on overpaid tax, will drop from 3.5% to 3.25%.

HMRC sets its late payment interest rate at the Bank of England base rate plus 4%, and its repayment interest rate at the base rate minus 1%, with a minimum floor of 0.5%.

HMRC sets its late payment interest rate at the Bank of England base rate plus 4%, and its repayment interest rate at the base rate minus 1%, with a minimum floor of 0.5%.

Paul Hornby, Managing Director at JF Hornby & Co, welcomed the news but urged businesses to keep things in perspective: “While any reduction in costs is a step in the right direction, it’s hardly a game-changer.

“Interest on late payments is still steep—and should be avoided where possible. This change highlights the importance of proactive cashflow management and getting your tax liabilities in on time.”

He added: “There’s also a temptation to celebrate when the repayment interest rate improves, but it’s worth remembering that you’re effectively lending HMRC your money. It’s far better to have it working for you within your business.”

The business community continues to watch closely for further rate changes as economic uncertainty, supply chain challenges, and inflationary pressures persist.

Many business leaders are now calling on the government to maintain a steady hand and avoid additional burdens during what remains a volatile trading environment.